The Hindu : Page 01

Syllabus : GS 2 : International Relations

The Supreme Court delivered a significant 8:1 judgment affirming that State Legislatures have the power to tax mining lands and quarries, independent of the Parliament’s Mines and Minerals (Development and Regulation) Act of 1957 (MMDR Act).

Case Background

- The case, Mineral Area Development Authority v. M/s Steel Authority of India, pending for over 25 years, was decided by an 8-1 split, with Chief Justice DY Chandrachud authoring the majority opinion.

Understanding Royalties and Taxes

- Royalties are fees paid for the right to use a product, distinct from taxes.

- Section 9 of the Mines and Minerals (Development and Regulation) Act, 1957 (MMDRA) requires leaseholders to pay royalties to those leasing the land.

Legal Questions and Historical Decisions

- The Supreme Court’s 1989 India Cement Ltd v. State of Tamil Nadu decision initially deemed royalties as taxes, a position challenged and revisited over the years.

- In 2004, State of West Bengal v. Kesoram Industries Ltd clarified that royalties are not taxes, correcting a typographical error from the India Cement decision.

- The Mineral Area Development Authority case sought to resolve conflicts arising from these interpretations.

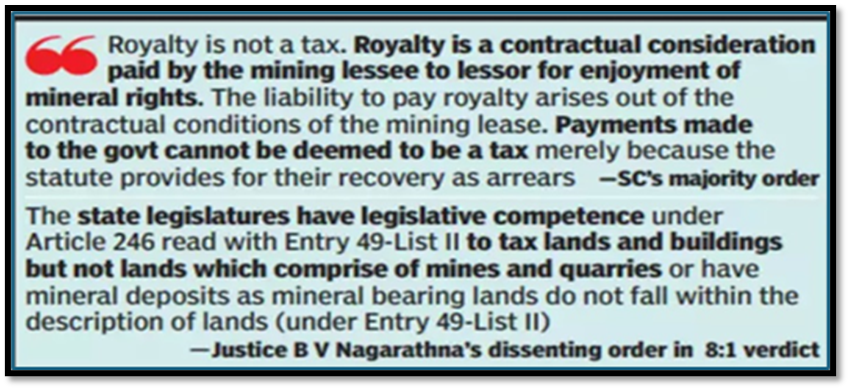

Majority Decision: Royalties Are Not Taxes

- The majority ruled that royalties are payments based on specific contracts between leaseholders and lessors, not taxes.

- Taxes serve public purposes, while royalties compensate lessors for exclusive mineral rights.

States’ Power to Tax Mineral Development

- The court held that states can tax mineral development activities, independent of the MMDRA, under Entry 50 of the State List, which grants exclusive state powers over mineral rights taxes.

- Entry 54 of the Union List grants the Centre regulatory power over mines and mineral development but not taxing power.

Dissenting Opinion by Justice Nagarathna

- Justice Nagarathna argued that royalties should be considered taxes to maintain uniform mineral development.

- She believed the MMDRA’s purpose would be undermined by allowing states to impose additional levies.

- She also contended that the MMDRA denuded states’ taxing powers post-enactment and that Entry 49 of the State List does not permit taxing mineral-bearing land.

Implications

- This ruling allows states to generate additional revenue through taxes on mining activities and land used for mining, providing clarity on the distinction between royalties and taxes and reinforcing states’ fiscal autonomy in mineral development..

UPSC Mains PYQ : 2014

Ques : Though the federal principle is dominant in our Constitution and that priniciple is one of its basic features, but it is equally true that federalism under the Indian Constitution leans in favour of a strong Centre, a feature that militates against the concept of strong federalism.